Insights and Analysis: Mortgage and Real Estate Capital Markets Update with Jeff Rosato, SVP of Capital Markets at Nationwide Mortgage Bankers.

Key Takeaways

Mortgage rates remained relatively stable last week despite continued economic strength, as easing concerns over inflation and lower oil prices helped improve sentiment in the bond market. While inflation remains above the Federal Reserve’s target, recent data met expectations, allowing the Fed to maintain its wait-and-see approach. Markets are now focused on upcoming employment reports, housing data, and ongoing geopolitical developments that could influence Treasury yields, mortgage-backed securities (MBS), and future interest rate decisions.

Here’s a look at this week’s update on the major bond market indices, scheduled Federal Reserve meetings, upcoming market-moving economic data releases, and general bond market trends.

Bond Market Indices

“The fear that geopolitical tensions would continue to fuel a surge in inflation were alleviated somewhat and that has helped reduce the expectations for Fed rate hikes in the near term.”

Market Overview and Rate Trends

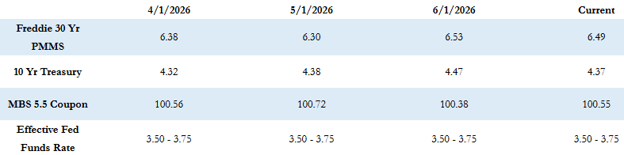

The Freddie Mac average 30-year fixed mortgage rate was 6.49% as of last Thursday, increasing just 2 basis points from the previous week. That places the maximum APR for 30-year fixed-rate loans at approximately 7.99% (6.49% + 1.50%).

Meanwhile, the 10-year Treasury yield closed the week at 4.37%, declining by approximately 8 basis points from the prior week.

Bond Market Performance & Federal Reserve Outlook

Treasuries and mortgage-backed securities (MBS) rallied for several consecutive days last week as oil prices moved lower. The easing of concerns that geopolitical tensions would continue driving inflation helped reduce market expectations for additional Federal Reserve rate hikes in the near term.

Economic data remained encouraging, with consumer income, business investment, and first-quarter GDP all posting strong results. Although inflation continues to run above the Federal Reserve’s 2% target, last week’s Personal Consumption Expenditures (PCE) Index came in exactly as expected, avoiding any upside surprise.

With economic conditions remaining solid and inflation concerns moderating, the Federal Reserve appears comfortable maintaining its current wait-and-see approach. At present, financial markets are pricing in approximately a 30% probability of a 0.25% rate hike in July, increasing to slightly above 50% for the September meeting.

Geopolitical uncertainty surrounding the conflict in Iran remains an important factor to monitor, as any renewed spike in oil prices could quickly impact inflation expectations, bond markets, and the Fed’s outlook.

Economic Calendar & Market Drivers

Although this week includes a shortened trading schedule due to the holiday, several important economic reports are scheduled.

Housing data began with the Case-Shiller Home Price Index. Attention shifts to employment, with the June ADP Employment Report, followed by the official U.S. Employment Report on Thursday.

As a reminder, financial markets will close early at 2:00 p.m. ET on Thursday and remain closed on Friday in observance of the holiday.

Current Market Conditions

MBS prices are generally flat compared to Friday’s close, while the 10-year Treasury yield remains unchanged at 4.37%.

Looking Ahead

Markets will continue to watch employment data, inflation trends, Federal Reserve expectations, and geopolitical developments for signs of where interest rates may head next. While economic fundamentals remain resilient, ongoing global uncertainty means mortgage rates and bond markets are likely to remain sensitive to new information. Staying informed on these developments will be essential as the market continues to navigate a changing economic landscape.