Insights and Analysis: Mortgage and Real Estate Capital Markets Update with Jeff Rosato, SVP of Capital Markets at NMB Now.

Key Takeaways

Mortgage rates and Treasury yields moved higher last week as renewed geopolitical tensions, persistent inflation concerns, and evolving Federal Reserve policy continued to shape financial markets. Investors are closely watching this week’s Consumer Price Index (CPI), Producer Price Index (PPI), retail sales, and comments from Federal Reserve officials for additional insight into the path of inflation and the likelihood of future interest rate changes. As volatility remains elevated, mortgage-backed securities and bond markets continue to react quickly to economic data and global events.

Here’s a look at this week’s update on the major bond market indices, scheduled Federal Reserve meetings, upcoming market-moving economic data releases, and general bond market trends.

Bond Market Indices

“The Fed remains concerned about the risk of renewed inflation pressures from higher energy costs, but will need more evidence that those pressures are becoming broader and more persistent before approving any rate hikes.”

Market Overview and Rate Trends

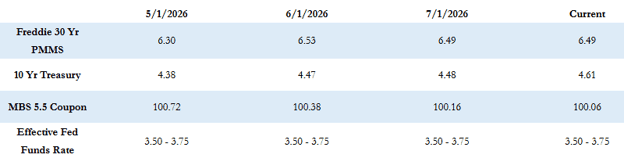

The Freddie Mac average 30-year fixed rate is at 6.49% as of last Thursday, up significantly by 6 basis points compared to the prior week. That puts the maximum APR this week for 30-year fixed-rate loans at roughly 7.99% (6.49 + 1.50). The 10-year Treasury yield closed last week at 4.57%, up sharply by approximately 11 basis points for the week.

Federal Reserve Policy and Global Market Developments

Last week, renewed hostilities near the Strait of Hormuz followed another breakdown in the fragile U.S./Iran ceasefire. These developments pushed oil prices higher and created volatility in the bond markets. Despite the week’s volatility, Treasuries and mortgage-backed securities finished Friday with a modest rally.

The minutes from the June FOMC meeting were also released last week. The committee remains dependent on fresh inflation data, and new Federal Reserve Chairman Kevin Warsh reiterated the Fed’s commitment to restoring price stability and bringing inflation back to its 2% target.

The minutes also revealed that the Federal Reserve will remove its explicit forward rate guidance, providing policymakers with greater flexibility while reaffirming their commitment to transparency regarding future monetary policy decisions.

The Fed remains concerned about the risk of renewed inflation pressures from higher energy costs but will need more evidence that those pressures are becoming broader and more persistent before approving any rate hikes. Currently, Fed futures markets are pricing in approximately a 40% chance of a 0.25% rate hike at the July meeting, with those odds increasing to roughly 75% by the September meeting. The consensus expectation is that the Fed will hold rates steady in July, though a September rate hike remains a realistic possibility if economic data continue to support it.

Economic Calendar and Market Drivers

This week’s focus shifts to new inflation data, with the Consumer Price Index (CPI) and the Producer Price Index (PPI) scheduled for release. Additional consumer data will also be released, including personal consumption and retail sales.

Federal Reserve presidents and governors are also scheduled to speak throughout the week. Market participants will be listening closely for commentary on the June FOMC meeting and how incoming economic data may influence decisions at the July meeting.

Because comments from Federal Reserve officials can significantly influence financial markets, and with renewed uncertainty in the Middle East, market volatility is expected to remain elevated throughout the week.

Current Market Conditions

Mortgage-backed securities are down approximately 25 to 30 basis points compared to Friday’s close, while the 10-year Treasury yield has increased a few basis points to 4.61%.

Looking Ahead

As markets continue to navigate persistent inflation concerns, evolving Federal Reserve policy, and ongoing geopolitical uncertainty, investors will remain focused on economic data and central bank commentary for clues about the direction of interest rates.

Stay tuned each week as we continue delivering insights on the markets and what’s moving them.