Insights and Analysis: Mortgage and Real Estate Capital Markets Update with Jeff Rosato, SVP of Capital Markets at NMB Now.

Key Takeaways

Mortgage rates edged lower last week as resilient economic data, easing inflation pressures, and declining energy prices helped stabilize bond markets. The Federal Reserve continues to take a patient, data-dependent approach to monetary policy, with markets closely watching upcoming inflation trends, economic growth indicators, and the next Federal Open Market Committee (FOMC) meeting on July 29. While geopolitical uncertainty continues to create market volatility, lower oil prices and steady labor market conditions have helped reduce inflation concerns and support a more stable mortgage rate environment.

Here’s a look at this week’s update on the major bond market indices, scheduled Federal Reserve meetings, upcoming market-moving economic data releases, and general bond market trends.

Bond Market Indices

“With resilient economic data and reduced inflationary pressures, the Fed remains comfortable in their wait and see data dependent approach to monetary policy and strategy.”

Market Overview and Rate Trends

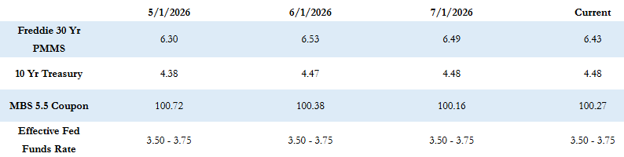

The Freddie Mac average 30-year fixed rate is at 6.43% as of last Thursday and was down significantly by 6 basis points compared to the prior week. That puts the max APR this week for 30-year fixed-rate loans at roughly 7.93% (6.43 + 1.50).

The 10-year Treasury yield closed last week at 4.48%, which was up sharply by about 11 basis points for the week.

Last week, Treasuries and mortgage-backed securities (MBS) finished the month slightly lower. MBS prices have stabilized recently, although some volatility remains in the bond markets due to ongoing geopolitical tensions in the Middle East.

Oil prices have decreased dramatically recently to less than $70 per barrel, which has helped stabilize markets and ease inflation concerns tied to energy costs.

Federal Reserve Policy & Economic Outlook

Recent economic data has shown that the economy remains resilient. While growth may be slowing, it is not stalling, as labor market data continues to remain strong. Lower energy prices have also helped ease recent inflation pressures that increased when oil prices surged.

With resilient economic data and reduced inflationary pressures, the Fed remains comfortable in its wait-and-see, data-dependent approach to monetary policy and strategy.

The key question for the Federal Reserve is whether economic growth is cooling enough to bring inflation down to its target level without triggering a broader economic downturn.

Currently, the market is pricing in approximately a 30% chance of a 0.25% rate hike in July, with that probability increasing to slightly over 50% for the September FOMC meeting. Those expectations can change as new economic data is released throughout July and markets continue to evaluate conditions leading up to the FOMC meeting on July 29.

Economic Calendar & Market Drivers

This week’s economic calendar is relatively light, with limited major market-moving data releases.

The primary focus will be on the release of the minutes from the June FOMC meeting, which are not expected to include any major surprises. Beyond that, markets will continue monitoring economic indicators and Federal Reserve commentary for additional insight into the future direction of monetary policy.

Current Market Conditions

MBS prices are generally flat compared to where they closed on Thursday, and the 10-year Treasury is also flat compared to Friday’s close at 4.48%.

Looking Ahead

Markets are expected to remain focused on incoming economic data, inflation trends, Federal Reserve policy signals, and geopolitical developments. With the Fed maintaining a cautious approach and economic conditions continuing to evolve, mortgage rates will likely remain sensitive to new information. Staying informed and prepared will be key as borrowers, lenders, and housing professionals navigate an ever-changing market environment.