Insights and Analysis: Mortgage and Real Estate Capital Markets Update with Jeff Rosato, SVP of Capital Markets at Nationwide Mortgage Bankers.

Key Takeaways

Mortgage rates remain elevated as persistent inflation, higher energy prices, and ongoing geopolitical instability continue to influence bond markets and Federal Reserve policy expectations. The market has largely embraced a “higher for longer” interest rate environment, with investors closely watching the upcoming June Federal Open Market Committee (FOMC) meeting, employment data, and inflation trends for signs of future rate movement. While consumers and the labor market have remained resilient, elevated borrowing costs and energy prices continue to shape mortgage rates, Treasury yields, and overall market sentiment.

Here’s a look at this week’s update on the major bond market indices, scheduled Federal Reserve meetings, upcoming market-moving economic data releases, and general bond market trends.

Bond Market Indices

“Interest rates have remained elevated over the last few months with persistent inflation and geopolitical instability being the main drivers of higher rates.”

Market Overview and Rate Trends

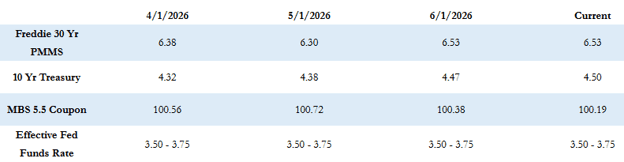

The Freddie Mac average 30-year fixed rate is at 6.53% as of last Thursday and was up just 2 basis points compared to the prior week but has increased sharply by 17 basis points over the past two weeks. That puts the maximum APR this week for 30-year fixed-rate loans at roughly 8.03% (6.53 + 1.50).

The 10-year Treasury yield closed last week at 4.45%, which was down by about 10 basis points for the week.

Federal Reserve Policy and Inflation Outlook

Interest rates have remained elevated over the last few months, with persistent inflation and geopolitical instability serving as the primary drivers of higher rates. Elevated oil prices continue to contribute to inflationary pressures, while the Federal Reserve has shifted toward a more neutral, and potentially hawkish, monetary policy stance.

The market is now operating in a “higher for longer” interest rate environment, with attention turning to the FOMC’s June meeting. This meeting will include an updated dot plot, providing insight into where Federal Reserve policymakers expect interest rates to be over the next several years. It will also mark the first FOMC meeting under new Federal Reserve Chairman Kevin Warsh.

Any upward revisions to the Fed’s rate projections would further reinforce the higher-for-longer narrative. While markets have steadily reduced expectations for near-term rate cuts, they have not yet begun pricing in a meaningful probability of future rate hikes.

Economic Conditions and Consumer Resilience

Despite ongoing inflationary pressures, the U.S. consumer has remained resilient, and the labor market continues to show strength. Higher energy costs and borrowing expenses have largely been absorbed by consumers, but the longer tensions remain elevated in the Middle East, the greater the risk that inflation could have a broader negative impact on economic growth.

Even if geopolitical tensions begin to ease, the lasting effects of sustained high energy prices may continue to contribute to persistent inflation.

Economic Calendar and Market Drivers

This week’s economic calendar is relatively light, but labor market data will be the primary focus. The May ADP Employment Report will be released on Wednesday, followed by the official May U.S. Employment Report on Friday, along with updates on the unemployment rate and consumer credit.

The Federal Reserve and market participants will continue evaluating incoming economic and inflation data. However, market movement is expected to remain heavily influenced by geopolitical developments until greater clarity emerges regarding ongoing conflicts and their impact on global energy markets.

Current Market Conditions

MBS prices are worse by approximately 25 to 35 basis points compared to Friday’s close, and the 10-year Treasury yield is up by about 5 basis points to 4.51%.

Looking Ahead

As markets move into June, investors will remain focused on Federal Reserve policy signals, labor market performance, inflation trends, and geopolitical developments. With interest rates continuing to respond quickly to economic and global events, staying informed about evolving market conditions will be essential for navigating opportunities and risks in the weeks ahead.