Insights and Analysis: Mortgage and Real Estate Capital Markets Update with Jeff Rosato, SVP of Capital Markets at Nationwide Mortgage Bankers.

Key Takeaways

Mortgage rates and Treasury yields remain elevated as inflation pressures, geopolitical instability, and resilient U.S. labor market data continue to drive a “higher for longer” Federal Reserve policy outlook. Markets are closely focused on this week’s inflation reports, including CPI and PPI, for confirmation of whether price pressures are stabilizing or remain persistent. With the Federal Reserve’s June FOMC meeting approaching, investors are weighing the potential for revised rate expectations and continued volatility in bond markets, mortgage-backed securities, and consumer borrowing costs.

Here’s a look at this week’s update on the major bond market indices, scheduled Federal Reserve meetings, upcoming market-moving economic data releases, and general bond market trends.

Bond Market Indices

“This week the focus will be back on inflation data with the CPI being released mid-week and PPI being released on Thursday.”

Market Overview and Rate Trends

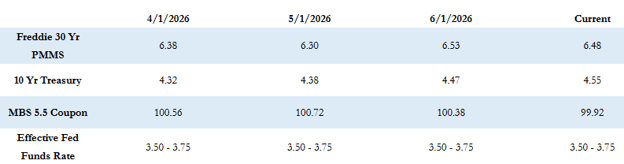

The Freddie Mac average 30-year fixed rate is at 6.48% as of last Thursday, down 5 basis points compared to the prior week. That puts the maximum APR this week for 30-year fixed-rate loans at roughly 7.98% (6.48 + 1.50). The 10-year Treasury yield closed last week at 4.54%, up sharply by about 9 basis points for the week.

Federal Reserve Policy and Inflation Outlook

Interest rates have remained elevated over the last few months, with persistent inflation and geopolitical instability being the main drivers of higher rates. Uncertainty in the markets remains as participants continue to balance resilient domestic economic data against inflationary risks tied to elevated oil prices stemming from the ongoing conflict in Iran.

Last week’s labor market data showed continued strength, with the May employment report surprising to the upside at 172,000 jobs created versus expectations of 80,000. Layoffs remain historically low, and the unemployment rate held steady at 4.3%. This stronger-than-expected data reinforces the Federal Reserve’s patient stance and supports the continued “higher for longer” policy outlook.

The upcoming June FOMC meeting will require policymakers to weigh whether persistent inflation could necessitate higher rates or whether economic growth will soften enough to justify future rate cuts later this year. This meeting will also be the first under new Federal Reserve Chairman Kevin Warsh and will include an updated dot plot of future rate expectations. Any upward revision in the Fed’s projections would further reinforce the higher-for-longer narrative.

Economic Calendar and Market Drivers

This week’s primary focus returns to inflation data, with CPI scheduled for release mid-week and PPI on Thursday. Expectations call for continued inflationary pressure, though there is some anticipation of moderation.

If inflation data prints in line with expectations, it would reinforce the narrative of resilient growth paired with sticky inflation—supporting the view that rate cuts may remain delayed and keeping the possibility of future rate hikes on the table.

Current Market Conditions

MBS prices are generally flat compared to Friday’s close, and the 10-year Treasury yield is up 1 basis point to 4.55%.

Looking Ahead

As markets move deeper into June, attention will remain firmly on inflation data, Federal Reserve signaling, and labor market resilience. With rate volatility continuing to respond quickly to economic releases and global developments, staying closely attuned to incoming data will be critical as investors navigate an evolving interest rate environment.

Stay tuned each week as we continue delivering insights on the markets and what’s moving them.