Insights and Analysis: Mortgage and Real Estate Capital Markets Update with Jeff Rosato, SVP of Capital Markets at Nationwide Mortgage Bankers.

Key Takeaways

Mortgage rates edged lower last week despite continued pressure from inflation concerns, elevated energy costs, and uncertainty surrounding geopolitical developments in the Middle East. The Federal Reserve held interest rates steady at its latest meeting but adopted a more hawkish tone, signaling that future rate hikes remain a possibility if inflation persists. Investors are now focused on upcoming Personal Consumption Expenditures (PCE) inflation data, consumer spending reports, and evolving oil market conditions, all of which could influence Treasury yields, mortgage-backed securities (MBS), and mortgage rates in the weeks ahead.

Here’s a look at this week’s update on the major bond market indices, scheduled Federal Reserve meetings, upcoming market-moving economic data releases, and general bond market trends.

Bond Market Indices

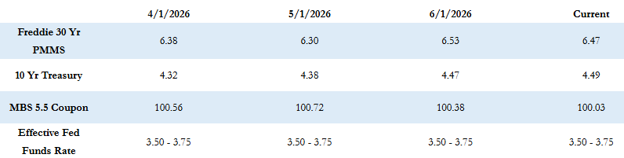

“As expected last week, the Federal Reserve FOMC left its benchmark Fed Funds rate unchanged in the 3.50-3.75% range.”

Mortgage Rate and Treasury Market Update

The Freddie Mac average 30-year fixed mortgage rate was 6.47% as of last Thursday, declining by 5 basis points compared to the prior week. That puts the maximum APR this week for 30-year fixed-rate loans at approximately 7.97% (6.47% + 1.50%).

The 10-year Treasury yield closed last week at 4.45%, up approximately 3 basis points from the previous week.

While mortgage rates moved modestly lower, financial markets remain highly focused on inflation trends, energy prices, Federal Reserve policy, and ongoing geopolitical developments.

Federal Reserve Holds Rates Steady but Adopts a More Hawkish Tone

As expected, the Federal Reserve’s Federal Open Market Committee (FOMC) left its benchmark Fed Funds Rate unchanged at 3.50%–3.75%. This marked the first interest rate decision under new Federal Reserve Chairman Kevin Warsh.

In the committee’s statement, Chairman Warsh reiterated that persistent inflation remains the Fed’s primary concern while economic growth continues to show resilience. The statement also suggested that policymakers are willing to pursue a more restrictive monetary policy if economic conditions warrant additional action.

As a result, market expectations for future rate hikes have increased significantly. Currently, investors are pricing in approximately a 35% probability of a 25-basis-point rate hike at the July FOMC meeting, with that probability increasing to slightly above 50% for the September meeting.

The shift in expectations has been driven largely by higher oil and energy costs resulting from the conflict with Iran, while key economic indicators—including retail sales, pending home sales, and labor market data—have generally continued to outperform expectations.

Geopolitical Developments and Oil Prices

Last week also brought the announcement of a U.S.-Iran memorandum of understanding aimed at ending hostilities through a ceasefire agreement and the reopening of the Strait of Hormuz for the safe passage of oil tankers.

Following the announcement, oil prices fell sharply to multi-month lows, closing the week at $76.60 per barrel.

Although there remains skepticism regarding the long-term stability of the agreement and the speed at which oil production and transportation can fully normalize, market participants generally view the development as a positive sign. Lower energy prices could help ease one of the most significant sources of recent inflation pressure.

For now, the Federal Reserve remains in a holding pattern. However, its recent communications suggest a noticeably more hawkish stance, indicating that the next policy move is more likely to be a rate hike than a rate cut if inflation remains elevated.

Economic Calendar and Market Drivers

The economic calendar begins the week relatively quietly, with limited major data releases scheduled until Thursday.

Key reports to watch include:

- Personal Income

- Personal Spending

- Personal Consumption Expenditures (PCE) Inflation Index

The PCE Inflation Index remains the Federal Reserve’s preferred measure of inflation and will likely play a significant role in shaping future monetary policy decisions.

Economists currently expect PCE inflation to increase for May, reflecting the impact of elevated oil prices and renewed inflationary pressures.

While consumer fundamentals have remained relatively stable, questions remain regarding how long consumers can sustain spending levels amid rising inflation and weakening real disposable income. As always, the Federal Reserve will remain heavily dependent on incoming economic data when determining future policy actions.

Current Market Conditions

Bond markets still remain under pressure. Mortgage-backed securities (MBS) prices are down approximately 25 to 30 basis points compared to Thursday’s close, while the 10-year Treasury yield has increased by roughly 5 basis points to 4.50%.

Looking Ahead

Markets are expected to remain highly sensitive to inflation readings, Federal Reserve commentary, energy prices, and geopolitical developments throughout the summer. As volatility continues across both bond and mortgage markets, staying informed about economic trends and policy developments will be essential for borrowers, homebuyers, and mortgage professionals navigating an evolving interest rate environment.