Insights and Analysis: Mortgage and Real Estate Capital Markets Update with Jeff Rosato, SVP of Capital Markets at Nationwide Mortgage Bankers.

Key Takeaways

Mortgage rates and bond markets remain range-bound as investors weigh persistent inflation risks driven by elevated oil prices against signs of slowing economic growth. Ongoing geopolitical tensions, particularly involving Iran, continue to influence energy markets and contribute to market volatility. With a packed economic calendar—including GDP, PCE inflation data, and the Federal Reserve’s April FOMC meeting—markets are closely watching for signals on future monetary policy. Expectations currently point toward a prolonged pause on rate cuts, keeping mortgage rates and Treasury yields sensitive to both economic data and global developments.

Here’s a look at this week’s update on the major bond market indices, scheduled Federal Reserve meetings, upcoming market-moving economic data releases, and general bond market trends.

Bond Market Indices

“The April FOMC meeting is also happening this week and the expectation is for no rate change on Wednesday.”

Market Overview and Rate Trends

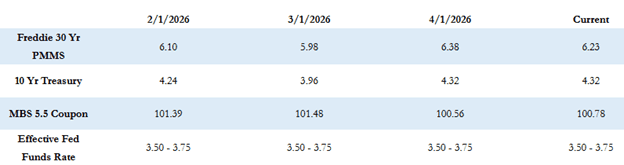

The Freddie Mac average 30-year fixed rate is at 6.23% as of last Thursday and was down fairly sharply by 7 basis points compared to the prior week. That puts the max APR this week for 30-year fixed rate loans at roughly 7.73% (6.23 + 1.50). The 10-year Treasury yield closed last week at 4.32%, which was up slightly by about 5 basis points for the week.

Inflation, Oil Prices, and Market Volatility

Over the past two weeks, mortgage rates and Treasury yields have remained in a tight range, with volatility easing slightly after spiking during the early stages of the conflict in Iran. The conflict has pushed oil prices higher, which is feeding directly into inflation and consumer costs.

Fluctuating oil prices remain the primary driver of day-to-day volatility in financial markets, including Treasury yields and mortgage rates. At the same time, market participants continue to balance inflation risks tied to elevated energy prices against the possibility of slowing economic growth and weakening labor market data.

Expectations for Federal Reserve policy have shifted significantly since the beginning of the year. Currently, markets are anticipating a prolonged pause on rate cuts, with Fed futures indicating only about a 25% chance of a 0.25% rate cut by year-end.

Policy Outlook & Economic Calendar

The economic calendar is particularly active this week. A range of housing market data will be released, including the Case-Shiller Home Price Index on Tuesday.

Markets will receive key updates including:

- Q1 2026 GDP data

- PCE inflation data

- Personal income and spending figures

The April FOMC meeting is also taking place this week, with expectations for no rate change on Wednesday. Chairman Powell will hold his final post-FOMC press conference at 2:30 PM on Wednesday before Kevin Warsh assumes the role of Chairman in May.

Current Market Conditions

MBS prices are worse by about 5–10 basis points compared to Friday’s close, and the 10-year Treasury is up slightly to 4.33%.

Looking Ahead

Markets are expected to remain highly sensitive to incoming economic data, Federal Reserve signals, and ongoing geopolitical developments. With inflation pressures still closely tied to energy prices and uncertainty surrounding global events, mortgage rates and bond yields will continue to react quickly to new information.

Staying informed and adaptable will be key as market conditions evolve in the weeks ahead.