Insights and Analysis: Mortgage and Real Estate Capital Markets Update with Jeff Rosato, SVP of Capital Markets at Nationwide Mortgage Bankers.

Key Takeaways

Mortgage rates and Treasury yields moved higher last week as the Federal Reserve reinforced its “higher for longer” stance amid renewed inflation concerns tied to rising oil prices and geopolitical tensions in Iran. With the Fed holding rates steady and signaling reduced likelihood of near-term cuts, markets are closely watching employment data and ongoing Fed commentary for direction. Volatility remains driven by energy prices and global uncertainty, keeping mortgage rates sensitive to both economic data and geopolitical developments.

Here’s a look at this week’s update on the major bond market indices, scheduled Federal Reserve meetings, upcoming market-moving economic data releases, and general bond market trends.

Bond Market Indices

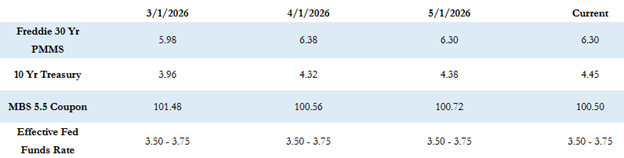

“As expected last week the FOMC held its benchmark Fed Funds rate steady in the 3.50–3.75% range where it’s been since the last rate cut in December 2025.”

Market Overview and Rate Trends

The Freddie Mac average 30-year fixed rate is at 6.30% as of last Thursday and was up fairly sharply by 7 basis points compared to the prior week. That puts the max APR this week for 30-year fixed rate loans at roughly 7.80% (6.30 + 1.50).

The 10-year Treasury yield closed last week at 4.38%, which was up by about 7 basis points for the week.

Federal Reserve Policy & Inflation Outlook

As expected, the FOMC held its benchmark Fed Funds rate steady in the 3.50–3.75% range, where it has remained since the last rate cut in December 2025. The committee reiterated its “higher for longer” stance as the probability of rate cuts later this year continues to decline.

The Fed has prioritized inflation risks over growth and employment concerns, particularly as rising oil prices have reignited inflation pressures. The committee noted an increasingly uncertain environment driven by the war in Iran, with geopolitical tensions and elevated energy costs contributing to the risk of persistent inflation.

This meeting marked Chairman Powell’s final session as chair, with Kevin Warsh now taking over the role. The committee was also divided, with four governors dissenting—one favoring a 0.25% rate cut and three opposing a cut but voting to remove the easing bias from the FOMC statement.

While the Fed remains concerned about inflation, it currently views the labor market and economic growth as stable. With renewed inflation pressures, Treasury yields have moved higher, and mortgage rates have followed suit. Mortgage rates have now increased for two consecutive weeks, impacting refinance activity, while purchase demand remains steady during the spring homebuying season.

Economic Calendar & Market Drivers

The economic calendar is busy this week. A range of housing market data will be released, but the primary focus will be on employment data, including the ADP employment report and the official U.S. Employment Report for April.

There are also numerous Federal Reserve speaking engagements scheduled, as governors and regional presidents provide further insight into last week’s policy decisions and the path forward.

Despite fresh economic data and Fed commentary, market movement is expected to remain heavily influenced by oil prices and ongoing uncertainty surrounding the conflict in Iran.

Current Market Conditions

MBS prices are worse by about 20–30 basis points compared to Friday’s close, and the 10-year Treasury is up sharply by 7 basis points to 4.45%.

Looking Ahead

Markets are expected to remain highly reactive to incoming economic data, Federal Reserve signals, and geopolitical developments. With inflation pressures closely tied to energy prices and uncertainty still elevated, mortgage rates and bond yields will continue to shift quickly as new information emerges—making it essential to stay informed and prepared to act in a rapidly evolving market.