Insights and Analysis: Mortgage and Real Estate Capital Markets Update with Jeff Rosato, SVP of Capital Markets at Nationwide Mortgage Bankers.

Key Takeaways

Mortgage rates remain near the 6% range, but market direction is currently being shaped less by traditional economic data and more by geopolitical developments and energy price volatility. Escalating tensions in the Middle East and disruptions to global shipping routes have pushed oil prices close to $100 per barrel, renewing concerns about inflation and contributing to a sharp rise in Treasury yields. At the same time, weaker labor market data has added uncertainty to the Federal Reserve’s policy outlook. With key inflation reports scheduled for release this week ahead of the Federal Reserve’s next meeting, investors and market participants are closely monitoring economic signals that could influence interest rate expectations and mortgage rate trends for the remainder of 2026.

Here is this week’s update on the major bond market indices, scheduled Federal Reserve meetings, upcoming market-moving economic data releases, and general bond market trends.

“As long as military operations continue and tensions remain elevated in the Middle East, markets will not be driven by any financial data points, but rather by the trajectory of geopolitical risk.”

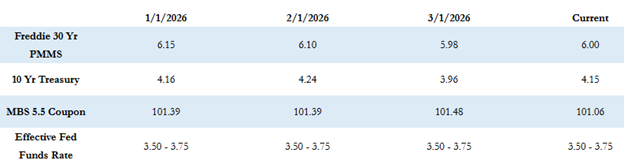

Market Overview and Rate Trends

The Freddie Mac average 30-year fixed mortgage rate stands at 6.00% as of last Thursday, which was up slightly by two basis points compared to the prior week. Based on that average, the maximum APR this week for 30-year fixed-rate loans is roughly 7.50%. The 10-Year Treasury yield closed last week at 4.13%, rising sharply by 17 basis points over the course of the week.

Mortgage rates had hovered around 6.10% for most of the year but moved closer to 6% about three weeks ago and have remained relatively steady since then. While rates have stabilized in that range for now, broader financial market movements continue to influence the outlook for both Treasury yields and mortgage-backed securities.

Geopolitical Risk Driving Market Sentiment

Since military operations in Iran began a little over a week ago, financial markets have been driven less by economic data and more by geopolitical developments. Tensions in the Middle East have included disruptions in shipping through the Strait of Hormuz, a critical global energy trade route. These disruptions have pushed oil prices sharply higher to just around $100 per barrel.

With the rise in oil and energy prices in general, there is renewed uncertainty surrounding the inflation outlook. Markets have significantly scaled back expectations for Federal Reserve rate cuts this year, including the possibility that the Fed may not cut rates at all for the remainder of the year. This shift in expectations has contributed to a major selloff in Treasuries, with the 10-Year yield rising sharply last week from below 4% to approximately 4.13%.

Federal Reserve Outlook

The Federal Open Market Committee meets next week and it is almost certain that policymakers will hold interest rates steady. However, futures markets are reflecting changing expectations for potential rate cuts later in the year.

The probability of a quarter-point rate cut at the April meeting is currently less than 10%. June is showing only about a 30% probability of a rate cut, while expectations for meaningful easing do not appear until September or October, where markets are pricing in better than a 50% chance of a cut. Futures markets are also reflecting roughly a 35% probability that interest rates remain unchanged through the end of the year.

As long as geopolitical tensions remain elevated, the path of inflation and energy prices will likely play an increasingly important role in shaping Federal Reserve policy expectations.

Labor Market Signals

Last week the February employment report was released and showed that the United States lost 92,000 jobs for the month, which was well below the expectation of a gain of 50,000 jobs. Employment figures for December and January were also revised downward, and the unemployment rate ticked up slightly to 4.44%, just above the expected level of 4.43%.

With the recent signs of softness in the labor market, it will be interesting to see how the Federal Reserve balances those concerns with the renewed inflation pressures stemming from higher energy prices. This combination of slowing job growth and rising input costs creates a more complicated policy environment for the central bank.

Economic Data to Watch

The economic calendar is particularly active this week as markets prepare for the next Federal Reserve meeting and rate decision. Inflation data will take center stage with the release of the Consumer Price Index on Tuesday and the Personal Consumption Expenditures Index, the Fed’s preferred measure of inflation, on Friday.

Additional reports scheduled for release this week include the U.S. Trade Deficit on Thursday, followed by the fourth-quarter GDP revision and the Consumer Sentiment report on Friday. These releases will provide important insight into inflation trends, economic momentum, and consumer confidence.

Current Market Conditions

Mortgage-backed securities prices are down slightly by approximately 5 to 10 basis points compared to where they closed on Friday. The 10-Year Treasury yield is generally flat compared to Friday’s close near 4.13%.

Looking Ahead

With geopolitical tensions rising, inflation concerns resurfacing, and key economic data scheduled ahead of the Federal Reserve’s next policy meeting, markets may continue to experience periods of volatility in the near term. Staying informed and closely monitoring both economic indicators and global developments will remain essential as investors and industry participants navigate the evolving outlook for interest rates and mortgage markets.

As always, we’ll continue monitoring market developments and economic data closely as the week unfolds.