Insights and Analysis: Mortgage and Real Estate Capital Markets Update with Jeff Rosato, SVP of Capital Markets at Nationwide Mortgage Bankers.

Key Takeaways: Bond Market Trends and Fed Outlook

Mortgage rates have remained stable, but upcoming inflation data and Federal Reserve speeches could drive market volatility this week. Meanwhile, January’s job report showed signs of a softening labor market, and newly proposed tariffs may add inflationary pressure, keeping rate cut debates open.

Here is this week’s update on the major bond market indices, scheduled Federal Reserve meetings, upcoming market-moving economic data releases, and general bond market trends.

Mortgage rates have been relatively unchanged and stable over the last few weeks, in line with the Fed’s wait-and-see approach to interest rates so far this year. That could change this week with the market-moving potential of Fed speakers and fresh inflation data coming on Wednesday with the Consumer Price Index (CPI) and Thursday with the Producer Price Index (PPI).

Lock Volume Trends

Last week was slightly above average for new lock volume to start the month. We had 93 locks totaling $44M, averaging 19 locks per day. Our trailing four-week daily lock average has increased back up to 18 locks per day. We finished January with 364 locks totaling $169.5M, reflecting a 10% increase compared to December. It’s great to see lock volume trending back up!

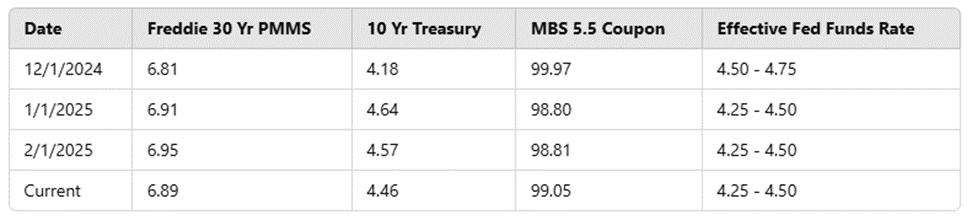

The Freddie Mac average 30-year fixed rate stands at 6.89% as of last Thursday, down 6 basis points from the prior week, marking the third consecutive week of declines. That puts the max APR this week for 30-year fixed-rate loans at roughly 8.39% (6.89% + 1.50%). Meanwhile, the 10-Year Treasury yield closed last week at 4.44%, down sharply by 13 basis points.

Employment Data and Market Impact

Last week, the spotlight was on the January employment report released on Friday. Nonfarm payrolls increased by 143,000, falling short of the expectation of 169,000. The report suggested some potential softening in the labor market, though the ADP private payroll report earlier in the week indicated that the labor market remains stable.

With the Federal Reserve closely monitoring employment trends, this mixed labor data keeps the debate open on the timing of future rate cuts. Additionally, the proposed Trump tariffs on goods from China, Mexico, and Canada could further complicate inflation pressures. Many analysts believe these tariffs will be passed on to consumers, raising already high prices and putting upward pressure on inflation.

Fed Policy & Market Outlook

Beyond current economic data, the Fed is also considering shifts in fiscal policy under the new administration. Specifically, the impact of the new Trump tariffs on consumer prices is a key focus. The FOMC will make their views known this week, with a full lineup of speaking engagements.

Additionally, Fed Chairman Powell will deliver his semi-annual monetary policy report to Congress on Tuesday and Wednesday. Mortgage rates have been stable in recent weeks, but this could change with the potential market volatility from Fed commentary and upcoming inflation data releases (CPI on Wednesday and PPI on Thursday).

Market Conditions Today

So far today, MBS prices are relatively unchanged from Friday’s close, while the 10-Year Treasury yield has risen slightly by about 2 basis points to 4.48%. Markets remain quiet for now, but the rest of the week has the potential for increased volatility starting tomorrow.

Stay tuned for market updates next week, as upcoming economic data and Fed commentary could bring new developments in rates and market trends.