Insights and Analysis: Mortgage and Real Estate Capital Markets Update with Jeff Rosato, SVP of Capital Markets at Nationwide Mortgage Bankers.

Key Takeaways

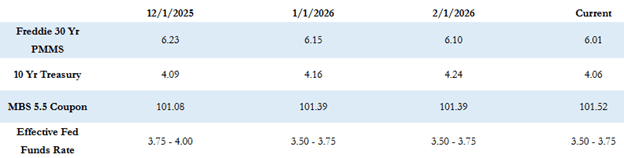

Mortgage rates edged lower this week, with the Freddie Mac 30-year fixed rate at 6.01% as bond markets improved and the 10-Year Treasury yield declined to 4.06%. Economic data remains mixed, with resilient labor trends, softer GDP at 1.4%, and PCE inflation at 2.9%. Markets are watching upcoming inflation data and Federal Reserve commentary closely, as expectations build around potential rate cuts later this year.

Here is this week’s update on the major bond market indices, scheduled Federal Reserve activity, upcoming market-moving economic data releases, and broader bond market trends.

“…Inflation data has shown that progress down towards the Fed’s target of 2% may be stalled a bit, and with the resilient labor market data the Fed may be shifting its focus back to inflation persistence and away from labor market weakness.”

Market Overview and Rate Trends

The Freddie Mac average 30-year fixed rate stood at 6.01% as of last Thursday, down eight basis points compared to the prior week. That puts the maximum APR this week for 30-year fixed-rate loans at roughly 7.51% (6.01 + 1.50).

The 10-Year Treasury yield closed last week at 4.08%, up four basis points for the week.

Mortgage rates have hovered around 6.10% for most of the year but moved closer to 6% by the end of last week. Economic data remains mixed. The labor market continues to show resiliency, with weekly jobless claims falling to 206,000. However, weaker pending home sales, slower retail activity, and wider trade deficits suggest there may be some headwinds to economic growth.

Fourth-quarter GDP was released last week and came in below expectations at 1.4%. The PCE inflation index was also released and registered 2.9% year over year, slightly above the 2.8% expectation.

Federal Reserve and Policy Outlook

Inflation data has shown that progress down towards the Fed’s target of 2% may be stalled a bit, and with the resilient labor market data the Fed may be shifting its focus back to inflation persistence and away from labor market weakness.

Fed funds futures markets show little chance of a rate cut at the March or April meetings. Currently, markets are pricing in roughly a 50% probability of a 0.25% cut at the June meeting, with approximately 0.625% in total cuts expected by year-end.

Monetary policy remains uncertain. Minutes from the January FOMC meeting indicated that some members remain open to rate hikes if inflation stays elevated, although Chairman Powell has suggested that the most likely next move would be a cut.

Additionally, new Fed leadership under Kevin Warsh, who is set to take over in May, introduces some policy uncertainty, though most expect continuity in the current approach. Geopolitical risks are also increasing, particularly with growing tensions involving Iran.

Economic Data and What to Watch

This week’s economic calendar is lighter compared to last week. Inflation data will be in focus on Friday with the release of the Producer Price Index (PPI).

There are also several Federal Reserve speaking engagements scheduled throughout the week, which could influence market sentiment.

Mortgage-backed securities are up approximately five basis points compared to Friday’s close, and the 10-Year Treasury yield is slightly lower at 4.06%.

Looking Ahead

With inflation data, housing metrics, and continued Federal Reserve commentary in focus, markets may remain sensitive to new information. Staying engaged and prepared will be key as economic conditions and policy expectations continue to evolve.

Wishing everyone a productive and successful week ahead.