Insights and Analysis: Mortgage and Real Estate Capital Markets Update with Jeff Rosato, SVP of Capital Markets at Nationwide Mortgage Bankers.

Key Takeaways

Mortgage rates moved higher this week as ongoing geopolitical tensions, particularly involving Iran, continue to drive volatility in energy markets and reinforce inflation concerns. Stronger-than-expected economic data signals that inflation remains persistent, leading markets to pull back expectations for rate cuts and consider the possibility of future rate hikes. With a light economic calendar ahead, attention will shift to commentary from the Federal Reserve and continued geopolitical developments as key drivers of market movement.

Here is this week’s update on the major bond market indices, scheduled Federal Reserve meetings, upcoming market-moving economic data releases, and general bond market trends.

“The dominant driver of financial markets right now is uncertainty around energy markets and how elevated oil prices will shape inflation expectations.”

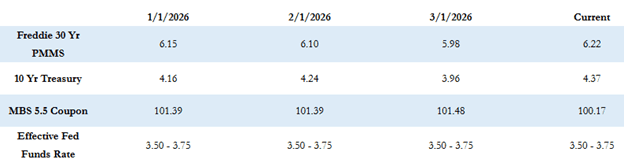

Market Overview and Rate Trends

The Freddie Mac average 30-year fixed rate increased to 6.22% as of last Thursday, rising 11 basis points from the prior week. This puts the maximum APR for 30-year fixed-rate loans at approximately 7.72% (6.22 + 1.50). Meanwhile, the 10-Year Treasury yield closed last week at 4.39%, also up 11 basis points.

Mortgage rates had hovered between 6.0% and 6.10% for much of the year, with relatively stable bond market conditions. However, volatility has returned following the escalation of geopolitical tensions involving Iran. Since the conflict began, mortgage rates have increased by approximately 20 basis points, reflecting broader uncertainty across financial markets.

Federal Reserve and Policy Outlook

Last week, the Federal Reserve held its benchmark interest rate steady, citing ongoing market uncertainty tied to geopolitical developments and inflation concerns.

Recent economic data has reinforced the narrative that inflation remains persistent. The Producer Price Index (PPI) came in higher than expected, signaling continued upward pressure on prices. As a result, expectations for rate cuts have shifted significantly.

Current Fed futures markets now indicate only about a 5% probability of a 0.25% rate cut by October, while the likelihood of a 0.25% rate hike has risen to approximately 15%. This shift reflects growing concern that sustained elevated energy prices could reignite inflation, potentially forcing the Fed to tighten monetary policy further.

At the same time, recent data suggests the U.S. labor market may be softening slightly. This combination of moderating employment conditions and persistent inflation has created a more complex outlook for monetary policy moving forward.

Geopolitical Developments

Geopolitical tensions remain the primary driver of market volatility. The ongoing conflict involving Iran continues to impact global energy markets, with elevated oil prices contributing to inflation concerns.

If these conditions persist, prolonged increases in energy costs could further disrupt bond markets and influence interest rate expectations. Until greater clarity emerges, markets are likely to remain sensitive to geopolitical headlines and energy price fluctuations.

Economic Data and What to Watch

This week’s economic calendar is relatively light, with no major market-moving data releases expected. However, several speaking engagements from Federal Reserve officials are scheduled, and investors will be closely listening for additional insight into the Fed’s outlook and policy direction.

With limited new data, market movement is expected to be driven more by geopolitical developments than traditional economic fundamentals. As of today, MBS prices are up approximately 15–25 basis points compared to Friday’s close, while the 10-Year Treasury yield has declined slightly to around 4.35%.

Looking Ahead

Markets remain highly reactive to geopolitical uncertainty and inflation signals, with energy prices playing a central role in shaping expectations. Staying informed and adaptable will be key as conditions continue to evolve and influence mortgage rates and capital markets.

Wishing everyone a productive week ahead with continued focus on navigating market shifts and opportunities.