Insights and Analysis: Mortgage and Real Estate Capital Markets Update with Jeff Rosato, SVP of Capital Markets at Nationwide Mortgage Bankers.

Key Takeaways

Mortgage rates and bond markets continue to be driven primarily by geopolitical uncertainty and inflationary pressures, particularly those related to ongoing tensions in the Middle East and volatility in oil prices. While U.S. economic data—including inflation readings and labor market indicators—continues to show mixed but generally resilient conditions, investors remain focused on how energy costs could reaccelerate inflation and influence Federal Reserve policy. As a result, mortgage rates, Treasury yields, and MBS performance remain highly sensitive to global developments and upcoming economic data releases, including inflation and producer price reports.

Bond Market Indices

“The markets are focused on what happens next with oil prices and the conflict in Iran, rather than on underlying market fundamentals. The longer the conflict drags on, the more lasting the effects of higher energy costs will be, putting upward pressure on inflation.”

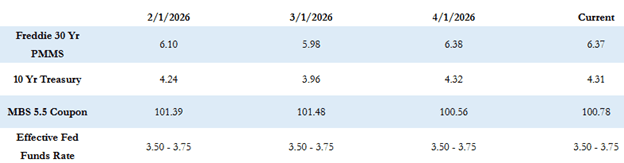

Market Overview and Rate Trends

The Freddie Mac average 30-year fixed rate is at 6.37% as of last Thursday, down fairly sharply by 9 basis points compared to the prior week. That puts the max APR this week for 30-year fixed-rate loans at roughly 7.87% (6.37 + 1.50). The 10-year Treasury yield closed last week at 4.31%, down slightly by about 3 basis points for the week.

Inflation and Geopolitical Drivers

The ongoing conflict in the Middle East has pushed oil prices higher, feeding directly into inflation and consumer costs. Fluctuating oil prices are the primary driver of day-to-day volatility in financial markets, including Treasury yields and mortgage rates. At the end of last week, the March CPI was released and showed that consumer prices jumped 0.9%, marking the largest month-over-month increase in several years. The spike was driven by a surge in energy prices. However, underlying inflation data showed that, aside from energy, most core inflation measures cooled to multi-month lows. In the short term, these mixed signals give the Fed reason for pause and patience. However, if high energy costs remain persistent and the conflict drags on, they will eventually bleed into broader inflation measures. Higher fuel prices will also push up the cost of other goods, including food and transportation.

Policy Outlook & Market Focus

Markets are focused on what happens next with oil prices and the conflict in Iran rather than on underlying market fundamentals. The longer the conflict persists, the more lasting the effects of higher energy costs will be, putting upward pressure on inflation.

There are several housing and inflation data releases this week, including the PPI and IPI. Additionally, multiple Fed officials are scheduled to speak, though market attention will remain centered on geopolitical developments and oil prices.

Current Market Conditions

MBS prices are up by approximately 10–15 basis points compared to Friday’s close, and the 10-year Treasury yield is down a few basis points to 4.30%.

Looking Ahead

Markets are expected to remain highly reactive to geopolitical developments, inflation data, and energy market volatility. Mortgage rates and bond yields will continue to reflect the balance between resilient economic fundamentals and ongoing global uncertainty. Staying informed and nimble will be key as conditions continue to evolve.

Wishing everyone a productive week ahead as we continue to monitor shifting market dynamics and opportunities.